Are Insurance Premiums Tax Deductible?

Insurance premiums are sometimes tax-deductible, but eligibility depends on the type of insurance, how the policy is used, and whether the expense is personal or business-related.

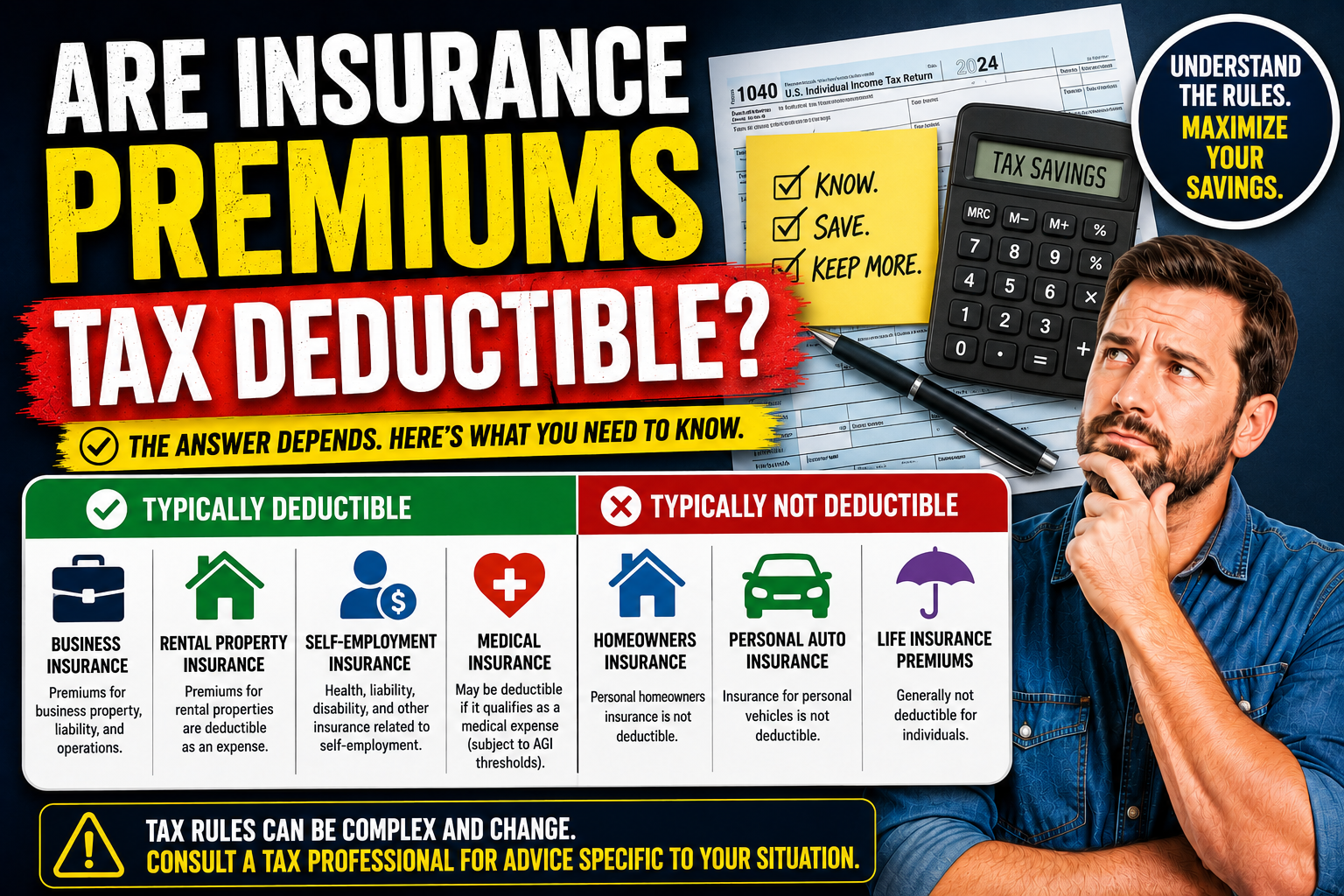

In most cases, personal insurance premiums — such as standard homeowners insurance or personal auto insurance — are not tax-deductible for federal income tax purposes. However, certain insurance costs related to business activities, rental properties, self-employment, or qualified medical expenses may qualify for tax deductions under specific rules.

Because tax laws can be complex and change over time, homeowners and business owners should understand which insurance premiums may qualify and which typically do not.

What Does Tax Deductible Mean?

A tax deduction reduces taxable income.

When an expense is deductible:

- The taxpayer may report it on a tax return

- Taxable income may decrease

- Overall tax liability may be reduced

Not every expense qualifies for deductions, and insurance premiums are subject to specific tax rules.

Are Personal Insurance Premiums Tax Deductible?

Most personal insurance premiums are generally not deductible for federal income taxes.

Common Non-Deductible Personal Insurance Policies

- Standard homeowners insurance

- Personal auto insurance

- Life insurance premiums

- Most personal renters insurance

- Mortgage protection insurance (in many cases)

These policies are usually considered personal living expenses.

When Insurance Premiums May Be Tax Deductible

There are several situations where insurance premiums may qualify for deductions.

Homeowners Insurance for Rental Properties

If a property is used as a rental or investment property, homeowners’ insurance premiums may often be deductible as a business expense.

Deductible Rental Property Insurance May Include:

- Landlord insurance

- Hazard insurance

- Fire coverage

- Liability insurance

Insurance expenses for rental properties are commonly reported as operating expenses.

Home Office Deductions

Self-employed individuals who qualify for a home office deduction may be able to deduct a portion of homeowners’ insurance premiums.

The deductible amount is generally based on:

- The percentage of the home used exclusively for business

Example

If:

- 10% of the home is used as a qualified office

then:

- Approximately 10% of homeowners’ insurance premiums may potentially qualify as a business expense.

Strict IRS home office rules apply.

Business Insurance Premiums

Business-related insurance premiums are often deductible.

Common Deductible Business Insurance Types

- General liability insurance

- Commercial property insurance

- Workers’ compensation insurance

- Professional liability insurance

- Commercial auto insurance

Businesses usually deduct these costs as ordinary operating expenses.

Health Insurance Premiums

Certain health insurance premiums may qualify for deductions under specific circumstances.

Possible Deductible Situations

- Self-employed health insurance

- Qualified medical expense deductions

- Long-term care insurance (subject to limits)

Eligibility depends on income, filing status, and IRS rules.

Mortgage Insurance Premiums

Mortgage insurance premiums may sometimes qualify for deductions depending on:

- Federal tax law changes

- Income limitations

- Loan type

This may include:

- PMI (Private Mortgage Insurance)

- FHA mortgage insurance premiums

Deduction availability changes periodically based on federal legislation.

Are Car Insurance Premiums Tax Deductible?

Personal auto insurance is usually not deductible.

However, deductions may apply when vehicles are used for:

- Business purposes

- Self-employment

- Rental activity

Only the business-use portion may qualify.

Insurance Premiums for Self-Employed Individuals

Self-employed individuals may have additional deduction opportunities.

Possible deductible insurance expenses may include:

- Health insurance

- Business liability insurance

- Commercial vehicle insurance

- Professional coverage

Business records and documentation are important.

Casualty Losses and Insurance

In limited situations involving federally declared disasters, uninsured losses may qualify for special tax treatment.

Rules surrounding casualty loss deductions are highly specific and may require professional guidance.

Common Insurance Premiums That Usually Are NOT Deductible

Personal Homeowners Insurance

Generally not deductible for primary residences.

Personal Vehicle Insurance

Typically considered a personal expense.

Life Insurance Premiums

Usually not deductible for individuals.

Title Insurance

Normally not deductible as a standard expense.

Most Personal Liability Policies

Generally treated as personal costs.

Important Tax Rules to Understand

Personal vs Business Use

Business-related insurance is more likely to qualify for deductions.

Documentation Matters

Taxpayers should keep:

- Premium invoices

- Policy documents

- Payment records

IRS Rules Change

Tax deduction rules may change over time.

State Taxes May Differ

State-level deductions sometimes vary from federal rules.

Tips for Managing Insurance and Taxes

Separate Business and Personal Expenses

Clear records help simplify tax filing.

Review Rental Property Expenses Carefully

Insurance costs may be deductible for investment properties.

Track Home Office Usage

Accurate measurements may support partiahomeowners ‘ insurance deductions.

Consult Qualified Tax Professionals

Tax laws can be complex and situation-specific.

Keep Organized Records

Documentation is important in case of audits or reviews.

Frequently Asked Questions

Is homeowners’ insurance tax-deductible?

Usually no for primary residences, but partial deductions may apply for qualified home offices or rental properties.

Can landlords deduct insurance premiums?

Often yes. Rental property insurance is commonly treated as a business expense.

Is car insurance tax-deductible?

Personal auto insurance is generally not deductible, but business-use portions may qualify.

Are health insurance premiums deductible?

Sometimes. Self-employed individuals and certain taxpayers may qualify under IRS rules.

Can mortgage insurance premiums be deducted?

Possibly, depending on current federal tax laws and income limitations.

Editorial Note

This article is intended for educational and informational purposes only. Tax laws, deduction eligibility, IRS rules, and insurance regulations change periodically and vary based on individual financial circumstances.

Disclaimer

This content does not constitute tax, legal, accounting, or financial advice. Individuals should consult qualified tax professionals, accountants, or legal advisors regarding insurance premium deductions and personal tax situations.

Final Thoughts

Insurance premiums are not always tax-deductible, especially when policies are primarily for personal use. However, certain business, rental property, self-employment, and qualified medical insurance expenses may qualify for deductions under specific tax rules. Understanding how insurance premiums interact with taxes can help homeowners, landlords, and business owners make more informed financial decisions and potentially reduce taxable income legally.